BITFINEX vs THE UNITED STATES OF AMERICA31 minuti

TL; DR: The image on the front page is a real photo of a fight between an antelope and a honey badger. The antelope lifts the honey badger with its horns and throws it 5 meters into the air. The honey badger gets up again, shakes off the dust, and resumes the attack.

[Thanks to The Cryptologist for the translation of this article]

1 – THE MANICHAEAN POWER OF THE BIEN-PENSANT

State of New York, 1921. In the aftermath of the First World War, the Big Apple became one of the world’s financial capitals, to the extent of challenging London’s dominance. At that time, the Federal Reserve Act 1913 had already created a monetary system leading to a strong increase in the money supply. Until the war, the U.S. economy had been punctuated with alternating inflation and deflation periods but the U.S. dollar had remained, overall, roughly stable in value. During the war, however, the annual rate of inflation of the U.S. dollar peaked at 15-17%. To protect themselves against inflation and due to the evolution or modification of social customs , investments and speculation in the stock and bond markets became common practice.

This speculative influx brought with it some of the worst examples of greed, and public opinion, in a society vulnerable to the musings of the media, it was easily influenced by news of scams, Ponzi schemes and financial cheats, so much so that it seemed incumbent on all institutions to remedy it. It was said that there are “hustlers who would sell shares of the blue sky if they could”. But scams and media coverage were not the only elements that pushed institutions to intervene – smaller bankers started to lobby, as they feared that current account holders would move more and more of their money from bank accounts to the financial markets.

Thus, the so-called “blue-sky law” set of laws which give exceptional powers to the Attorney General, with the aim of combating fraudulent financial activities, spread in various American states. In line with this, in 1921 the Martin Act was enacted in the State of New York.

At first, the Martin Act was a milder law than other American blue-sky laws, but over the years it began to have more aggressive applications, especially thanks to the interpretations of the Supreme Court in 1926. It thus became an increasingly powerful weapon in the hands of the Attorney General of New York, turning into what has since been called “the worst law in America”, at least according to the Wall Street Journal paper entitled, precisely, “The Worst Law in America”[1].

There are a lot of questionable aspects to the Martin Act. These include the fact that in order to proceed, the prosecutor does not need to prove that there is fraudulent intent, nor does it need to prove that there is any actual fraudulent trading occurring nor damage resulting from fraud (“probable cause”). Nor does it need to provide any details of the investigation (the rationale for such confidentiality would be to avoid reactions from the markets). In short, the prosecution has a “carte blanche” to operate “so far as possible” as long as it adheres to its ”beneficial purpose” of combating potential fraud, with an instrument that pushes the limits of what can be considered constitutional. The prosecutor can launch a subpoena to force witnesses to testify and provide documents useful to the investigation and, with the Martin Act, his decision to conduct the investigation cannot be reviewed by a court.

It should be noted that the Attorney General is an elective office, therefore a political office, selected by popular vote. Since January 1, 2019, Letitia James, an African-American activist in the Democratic Party, has been in office, elected with 3.7 million votes. Keep this person in mind, as we’ll come back to her shortly. It is she who today is responsible for the management of a power as great as that provided by the Martin Act.

For at least 75 years, this formidable and dangerous weapon of the U.S. regulator has been buried and forgotten. However, the financial crisis of 2008 was an excellent excuse to awaken the sleeping giant and for the New York Attorney General, it has become almost fashionable to use it in the last decade, perhaps also because of the personal advantages that, in some cases, they were able to obtain as a result. According to a Bloomberg article, by applying the Martin Act, the New York Public Prosecutor’s Office gained considerable visibility by imposing fines in the billions of dollars, hitting various Wall Street companies in cases where other regulators were stifled and had their hands tied[2].

The Attorneys general who have been in charge of the prosecution over the years have gone a little too far, abusing the Martin act for any purpose, even to investigate climate change; a subpoena was even issued to ExxonMobil which required a series of documents from the ’70s, in order to understand if the company had tried to hide the negative impacts of the oil business on “climate change”. Regarding Letitia James, she is the protagonist of the investigations about:

- the family owners of a pharmaceutical company using opioids (see here)

- Facebook on the users’ email collection and data privacy (see here)

- The finances of the National Rifle Association (see here)

- Donald Trump. Letitia refers to him as the “illegitimate president” (see here)

In short, it would seem that some investigations are guided by a strong political motivation, rather than a strictly legal one. According to articles by Bloomberg and Overlawyered, the investigations were used by prosecutors for their media appeal[3], with the aim of winning elections to government offices – “[They] call the law a license to extract huge payments from companies to glorify politicians and help ambitious Attorneys General win election to higher office”.[4].

This long introduction to the Martin Act will come in handy shortly, but let’s get to the present day. The world of cryptocurrency has been under the radar of the New York Public Prosecutor’s Office for some time now. Eric Schneiderman, who, to be clear, gave the subpoena to ExxonMobil on climate change, also issued a subpoena to Bitfinex in November 2018, about which my readers are already well informed.[5]

It must be said that the State of New York has proved totally hostile to the crypto world on several occasions. In August 2015, BitLicense came into effect, which involved the “Great Bitcoin Exodus”. We speak here of “exodus” because few companies were willing to operate in New York when having to pay between 50 and 100 thousand dollars to obtain such a license. Above all, however, what discouraged companies was the obligation, required for the license, to provide the regulator with an incredible amount of sensitive data relating to their business and their customers. So Bitfinex, Kraken, LocalBitcoins, Poloniex, Genesis Mining and many other companies stopped operating in the state. Ripple (which is a company, by the way!), Coinbase, Xapo and Bitpay are examples of those that have bought the license and remained.[6]

By 2016 Bitfinex had already been fined by the Commodity Futures Trading Commission (CFTC) because the platform grants, according to American laws, too much freedom in margin trading. Those who know and practice leveraged trading will understand well the futility and hassle of laws such as these applied by the CFTC. They seem to be intent on draining resources, or for the sole purpose of showing that they are the authority, which can arbitrarily restrict your freedoms. Nevertheless, even with the U.S. acting as a nanny by limiting margin optionality, investors are still perfectly capable to risk and lose everything.

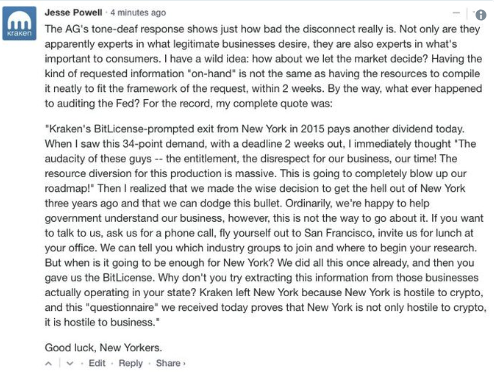

Regulators and prosecutors seem to be relentlessly targeting the Bitcoin ecosystem. Former prosecutor Schneiderman in 2018 investigated at least thirteen major exchanges including Coinbase, Bitfinex, Gemini and Kraken, presenting each company with a list of questions, in 34 points, to be completed and delivered within only 2 weeks.[7]

While some companies, including Bitfinex, were more accommodating, Jesse Powell of Kraken, tired of wasting time, money and having to change the road-map of his business because he was busy answering, within two weeks, a questionnaire that is more like an interrogation, decided to answer with the middle finger – “the prosecutor shows to be completely disconnected from reality […] we made the wise decision to leave New York three years ago […] go and ask for information from companies operating in his state. The questionnaire we received today proves that New York is not only hostile to crypto, but is hostile to business, in general”.

But why this new Manichean trend against cryptocurrency? These ‘bien-pensant bureaucrats’ rely on the consent of the voters and their superiors, they play on the emotional strings of the masses, praise for rebellion and they slavishly follow a sovereign morality that makes coercive violence a standard in its “modus operandi”. And what could be easier for a prosecutor who wants to make a career than to strike at the heart of the emerging Bitcoin ecosystem, to attack the “corrupt” world of cryptocurrencies, useful only for money laundering, wild speculation, or to finance black-hat hacker organizations and “terrorists” like Wikileaks? After all, the reasons for this hostility are not very different from those towards two famous characters, somehow linked to the Bitcoin world – Ross Ulbricht[8] and Julian Assange – a hypocritical and respectful morality and a lot, a lot of ignorance.

Bitcoin exchanges are the perfect scapegoat for all the evils of civilization – fragile and poorly structured, but always in business. If you trample on them, nobody stands up for their rights, let alone those of their users. Stories of money laundering and links with drugs only stoke the prejudice from our ‘benevolent friends’, and the recent words of the great scholar Joseph Stiglitz served as the most naïve incarnation of this – “we should shut down the cryptocurrencies”.

Above all, however, it seems this is a convenient time to target crypto exchanges, because for months now something very disturbing has been happening with some of them…

2 – INSOLVENT, INSOLVENT, INSOLVENT

In January 2019, Zerononcense, the research and consulting platform, with a focus on bitcoin and blockchain technology, sounded the alarm that a black swan event may be around the corner.[9] The warning being that certain exchanges seemed to be insolvent – not “exit scams” nor other forms – but something structurally deeper.

COINAPULT:

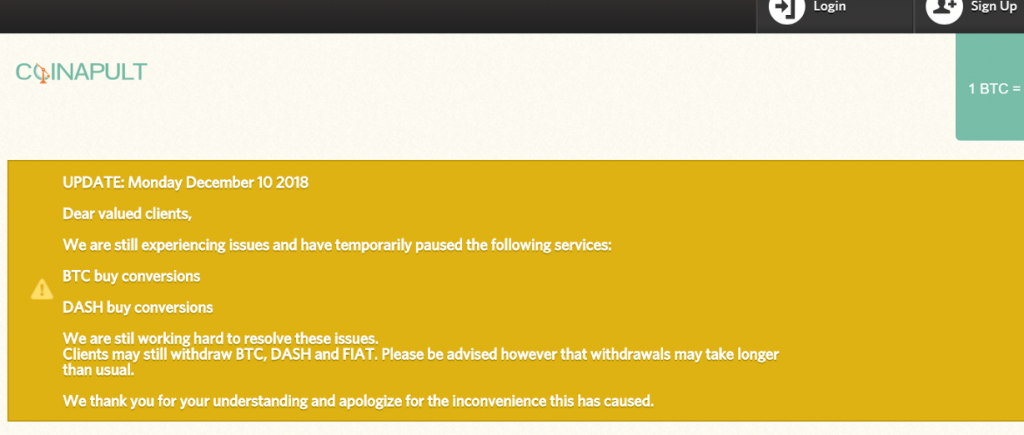

CCoinapult is a little-known exchange founded by Erik Vorhees of Shapeshift and launched with a seed investment of $750,000, some of which was contributed by Roger Ver. For months, however, users of Coinapult complained that their funds were blocked.[10]

On 10 December 2018, a message appeared on the homepage of the exchange, informing users that some services were “temporarily” suspended and withdrawals may take longer than usual to execute.

The payment processor Coinapult relies on is the Panamanian company known as Crypto Capital.

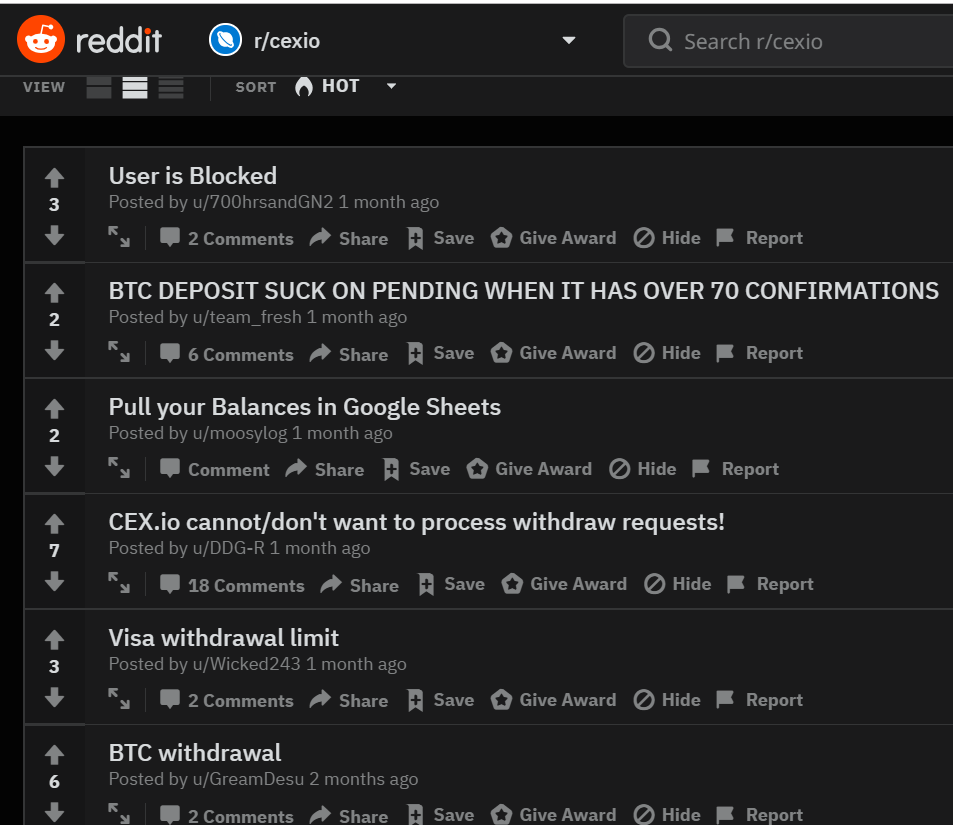

CEX.IO:

Coinapult is not an isolated case, with a similar fate falling on the exchange CEX.io. Users of CEX.io began experiencing problems with withdrawals as early as April / May 2018. There were also numerous complaints on twitter and reddit. For example, these users[11] waited 44 days to collect $34,000. The company justified itself by saying that it had encountered “difficulties in making transactions in dollars because of the unsatisfactory service of its payment processor, which had violated contractual terms and guarantees”.

Once again, the payment processor of CEX.io is the Panamanian company Crypto Capital.

CEX’s Reddit Channel:

CEX website:

QUADRIGA CX:

The story of QuadrigaCX is more and more turbulent, but it’s so theatrical that it’s worth highlighting every act, even at the risk of wandering a little from the goal of this article. The owner of the exchange, Gerald Cotten, has made crypto headlines all over the world because in December last year he “passed away”, taking 25,000 Bitcoins with him, of which only he had the private keys. But the real story behind it is even more incredible.

QuadrigaCX relied on a payment processor called Costodian Inc. (http://costodian.com/), which operated a bank account with the Canadian Imperial Bank of Commerce (CIBC). This bank, however, had doubts about the activities of the payment processor and being concerned about money laundering, froze the funds of Costodian Inc. as well as those of owner Jose Reyes, explaining that before releasing them they would need to confirm exactly who the money belongs to; whether to Jose and his company, QuadrigaCX, or to customers of either service.

The frozen funds total 28 million Canadian dollars (US$ 22 million) and of these, QuadrigaCX claims ownership of at least 16.3 million US dollars, of which it has attempted to recover, and have released, through legal action. After about 10 months of investigations, on November 9 2018, the Ontario Supreme Court ruled that it was not possible to establish ownership of those funds, which were subsequently seized and passed into the possession of the Court itself.[12]

As of yet, to this day, that money has still not been unlocked. But the best bit is yet to come. During 2018, QuadrigaCX continues to operate, and since Costodian Inc. is now unusable, they rely, yes, on Crypto Capital.

A Quadriga executive will later admit, through a post on Reddit in January, that since November 2018 the exchange had faced liquidity problems, but not so much because of the funds being blocked by the Supreme Court, but instead due to the fault of Crypto Capital. Meaning they were forced to remove Crypto Capital’s as a mode of deposits and withdrawals[13]:

Be careful to the timeline:

- On November 9, the Supreme Court ruled that it was impossible to determine whose money was in the bank. In short, it is not known if they belong to QuadrigaCX, its users, Costodian Inc. or some other entity

- QuadrigaCX experienced deposit and withdrawal issues during the course of the month due to Crypto Capital

- On 27 November, Gerald Cotten made his will and testament. He leaves almost everything to his wife, who he had only married the month before. Among the inherited assets, there is also a Lexus from 2017, an airplane and a yacht. But the will[14] is so detailed to the point that it also includes $100,000 left to a trust with the purpose to take care of his beloved Chihuahuas – Nitro and Gully[15]

- On December 9, 12 days after the drawing up of the will, Gerald Cotten “died” in India.

According to the reports, no other employee of the exchange knew the private keys, meaning that along with Cotten, around 26,500 bitcoins were lost (as well as other, smaller crypto currencies) belonging to around 90,000 QuadrigaCX customers. In fact, according to the analysis of transactions on the blockchain made by ZeroNoncense, there were less than 1000 BTC in the exchange wallets. So why are we talking about 25,000? So where did all the users’ money go? Are they in bitcoins or dollars? Are they frozen by the Supreme Court? Did Crypto Capital have them? Or, perhaps, did Nitro and Gully eat them?

The cause of death was determined to be complications of Chron’s disease. Whilst it is believed that Gerald Cotten really did die, with the body being repatriated to Canada, there are some people who remain skeptical. The Times of India report that there are many cases of fraudulent death certificates being made in the region, with six manufacturers having been arrested in just one month. If Gerald was so prudent, or if he felt that he was about to die, one wonders why he should draw up such a detailed will, catering even to his pet Chihuahuas, whilst completely forgetting the private keys of the bitcoins, whose safe management, should have been his top priority as a professional.

In short, what happened with Cotten is difficult to determine, but what is for certain is that Crypto Capital has contributed to the problems faced by the exchange, which has since gone bankrupt due to insolvency.

BTCC, CHIP-CHAP & BITFINEX:

In 2018 (the screenshot dates back to 28 January) the ‘partners’ page on Crypto Capital’s website listed several exchanges. However, we have seen that QuadrigaCX, Coinapult and CEX.io have suspended their services. Three other exchanges, Bitfinex, Chip Chap and BTCC left Crypto Capital and were removed from the page (seen in the screenshot below, marked with an orange cross). Evidently, they all had problems with the payment processor. Of those remaining on the current page, three no longer operate or otherwise do not offer deposit/withdrawal services (the aforementioned CEX, QuadrigaCX and Coinapult, all having become insolvent). Of all Crypto Capital’s customers, only EXMO seems to remain. See how the Crypto Capital site looks today: https://cryptocapital.co/#EXCHANGES

EXMO

EXMO is not a particularly well-known exchange and does not seem to have had any significant problems. The only major news was the kidnapping in 2017 of manager Pavel Lerner. At that date, the exchange had around 100,000 active traders. Pavel was kidnapped in Kiev by a group of men with balaclavas as he left his office. After paying a ransom of one million dollars in bitcoin, he was freed by the kidnappers, on a highway. This incident does not seem to have affected the exchange, and it seems that Pavel did not have any personal keys to access the exchange funds.

The company recently confirmed to me that it is still possible to use the Crypto Capital channel, although the EXMO site shows other channels for depositing and withdrawing funds, so it is likely that they mainly use alternatives. I doubt that, being a small exchange, they have yet noticed the problems of Crypto Capital. Or, since EXMO mainly serves customers in Eastern Europe, Crypto Capital could rely on banks with which it still manages to operate.

At this point of the investigation, it has become very clear that there is something deeply amiss with Crypto Capital, with similar issues replicated across many services resulting in disastrous consequences, all of which suggests that the analysis of Zerononcense was correct.

But why did all these exchanges rely on Crypto Capital? What company is this and what went wrong? Crypto Capital, originally a Panamanian company, ceased to be so in June 2018, when it moved to Zurich under the new name of Global Trade Solutions AG, authorized by Finma Switzerland to operate as a money service operator https://www.arif.ch/Members-list

This company has a bank account at the large British bank HSBC, while the subsidiary Global Trading Solutions LLC also has accounts in Citibank, Enterprise Bank & Trust and Wells Fargo. But there are at least 5 other companies belonging to the same group operating in Poland, Portugal and Germany. So how can we blame an exchange for having finally found, and subsequently use, a payment processor authorized to operate as such by the relevant institutions, that is crypto-friendly and that has so many connections and banking channels all over the world? It sounds like crypto heaven to any exchange in the space. Kraken and Binance also used Crypto Capital for a short time.

However, something has been wrong since at least January 2018. In the Netherlands, for example, the company has an account with ING Bank. The account was frozen in January 2018, but Crypto Capital managed to unblock the funds 112 days later. Perhaps it is just a coincidence, but during 2018 the Dutch bank ING wasn’t doing very well and in September it paid a fine of 775 million euros for failing to take measures against money laundering and corruption, and in October, Bankitalia (the Italian regulator) prohibits ING to open new bank accounts in Italy.

Then, in March, came the news from Poland, where Crypto Capital has two subsidiaries. $1.27 billion was seized by the authorities. At the time, there was still no formal accusation, but it was already known that Polish magistrates were awaiting information from Europol and Interpol, demonstrating that the investigation was on an international scale. Some articles talk about money laundering and criminal activities, with even the surprising suggestion of being linked to the Colombian drug cartel. There is, of course, zero evidence to back up those claims, however, a little folklore never hurts the newspapers. According to some reports, part of the money was linked to people whose names appeared on Panama Papers, i.e. in the documents of the tax havens made available after the leakage of data from the tax and legal office of Mossack Fonseca, from Panama. In the crypto world, the news of the seizure in Poland has a certain resonance, given that over 300 million of the funds seized at the two Polish subsidiaries of Crypto Capital, actually belong to Bitfinex customers, who sent their funds there, in order to use the exchange.

Then came Crypto Capital’s account in HSBC England, closed for fraud and money laundering in October 2018. Again, the news is linked to Bitfinex, although formally HSBC is not a bank of Bitfinex and has no agreement with the exchange. Bitfinex is however the most visible, simply because it is the largest of Crypto Capital’s customers, being the first to trade Bitcoin against the dollar.

Looking at the various companies in the group, it seems that no one has been spared.

- Haparc B.V, Netherlands – Bank ING (frozen in January 2018, funds returned 112 days later)

- Crypto SP z.o.o, Polonia – Cooperative Bank in Skierniewice (seized in March 2018)

- iTran SP z.o.o, Poland – Bank Zachodni WBK (seized in March 2018)

- Global Trading Solutions LLC, United States – US Bank (closed)

- Global Trade Solutions A.G., Switzerland – Caixa Geral De Depósitos, Portugal (closed)

- Global Trade Solutions GmbH, Germania – Deutsche Bank Private and Business Customers AG (?)

The account in Germany is perhaps the last to close, which could explain why EXMO is still operational through Crypto Capital. We have yet to find out, but probably, if it’s still operational, it’s days are numbered.

On 4 May, just a few days ago, we reached the end of this story – two arrest warrants for the African-American Reginald Fowler and the Israeli Ravid Yosef, from Tel Aviv. Fowler was a professional American football player, now co-owner of the Minnesota Vikings team. Also owner of Spiral Inc. (bankrupt), the OEM Logistics company, as well as many of the Crypto Capital group companies mentioned above. Ravid Yosef is a blogger and relationship coach from Los Angeles who settled in Tel Aviv and, according to articles, found the love of her life in a pub (a handsome black guy) while she was on a first date with someone else she found on Tinder. Indispensable details these.

Fowler is now under arrest whilst Yosef remains a fugitive.

The Crypto Capital investigation was conducted by the Southern District of New York (SDNY) and apparently the prosecutor’s office is targeting the entire crypto world, suspicious of any activity and service related to cryptocurrencies, not just those connected to Crypto Capital. The US authorities have, so to speak, and ‘easy target’, in spite of our financial freedom. Because after all, all the money blocked in the various accounts does not so much belong to Fowler and Yosef, but to unsuspecting exchanges and ordinary users. It is no coincidence that Bitcoin has grown by 15% in the last month – if the dollars are not safe, better to convert to bitcoin!

It is impressive how easily Americans are able to cross and dictate law outside their perimeter. This is not just about the crypto world. For example, at the end of April this year, after six years of investigations by the New York Department of Financial Services and other American authorities, Unicredit agreed to pay a $1.3 billion fine. The accusation is that of transactions with countries such as Iran, Libya, Syria, Cuba, Myanmar and Sudan, against which the United States has launched (often unilaterally) an embargo. It is striking how an embargo issued by a country can dictate the law on what private companies from other countries can and cannot do. Unicredit is by no means the only case, as many as 15 European banks have paid more than 19.5 billion dollars for violating embargoes and US sanctions against various countries. For example, BNP Paribas paid 9 billion in 2014. The list of other banks fined by the US authorities is incredibly extensive, including HSBC, ING or Barclays (the support bank of Coinbase).[16]

3 – LETITIA CONTRO BITFINEX

Last but not least, comes the most important part of this story, in which we all have a vested interest – given that many bitcoiners have an account on Bitfinex. The current Attorney General of New York (NYAG), Letitia James, is still willing to go after the company, but in the absence of evidence or “probable causes”, on what grounds could she sue the exchange? In this witch-hunting, an even older law of McCarthyism has come in handy: the infamous Martin Act. In the absence of evidence, the prosecution cannot bring a criminal case, so the court order dated April 24 is formally a preliminary[17] injunction that exploits the very law passed in 1921.

With this injunction, the Department of Justice requires Bitfinex to provide a series of documents relating to customers, transactions, accounts, tax filings, etc. and requires Bitfinex to identify each and every New York “Investors” on the platform. Finally, it orders the exchange to terminate the “alleged fraudulent practices”, which are only alleged, precisely, in the absence of evidence. The mere possibility seems sufficient for the NYAG to be granted an order of this kind, with a potentially detrimental effect on the company itself, its reputation, but also the markets. All this without even contacting the company privately first: “without notice or a hearing”, as Bitfinex complains in the public response announcement. The justification for such an immediate injunction would be, according to the prosecution, that a potential “dissipation of assets” by Bitfinex or Tether would make an ex post refund impossible, should the fraud be proven.

The factual accusation against Bitfinex is that the company tried to cover, thanks to US$ 700 million in Tether’s assets, the “apparent” loss of approximately US$ 850 million of Bitfinex client funds to Crypto Capital and failed to disclose the withdrawal difficulties they were experiencing on the platform, to both their shareholders and customers.

“Bitfinex … engaged in a cover-up to hide the apparent loss of $850 million dollars”.

The prosecutor alleged that Bitfinex failed to recover those funds from Crypto Capital, their payment processor. Among the files produced by the Office of the NYAG, are some chats, dated August 2018, in which Giancarlo Devasini (with the account “Merlin”) puts pressure on an executive of Crypto Capital, warning him about the risks of a systemic disaster if he does not release the funds:

Merlin, 15.08.2018 10:01:

I need to provide customers with precise answers at this point, can’t just kick the can a little more

Merlin, 15.08.2018 10:02:

Please understand all this could be extremely dangerous for everybody, the entire crypto community

Merlin, 15.08.2018 11:03:

BTC could tank to below 1k if we don’t act quickly

Merlin, 15.08.2018 11:46:

Hey Oz, sorry to bother you every day, is there any way to move at least 100M … ? We are seeing massive withdrawals and we are not able to face them anymore unless we can transfer some money out of Cryptocapital

Despite all this, Bitfinex somehow managed to save face (and avoided further dumping of the price of bitcoin and a systemic crisis, in full bear market) by responding to the needs of users through the execution of 700 transfers for more than a billion dollars in October 2018 alone. These withdrawals were made by large investors, given the amounts, for an average of one and a half million dollars per transfer.

In November 2018, however, Bitfinex faced a new wave of transfers and Crypto Capital was still silent. You can’t see the money and Devasini is on a rampage, writing to the executive of Crypto Capital:

Merlin, 28.11.2018 10:55:

I think you should stop playing and tell me the truth about what is going on

Merlin, 28.11.2018 10:56

I am not your enemy, I am here to help you and have been very patient so far, but you need to cut the crap and tell me what is going on

Bitfinex claims to have willingly provided these chats to the prosecution with a view to facilitate collaboration, since there is nothing to hide. A “Good deed” that may have turned against them. They did not expect the ex parte injunction dated April 24. Perhaps Kraken’s “middle finger” strategy would have been better?

Since October 2018, Bitfinex has started legal proceeding trying to recover the money. Given the fact that Crypto Capital could not return the funds (and we now know very well why), Bitfinex turned directly to the banks in which the funds are located.

As we will see, Bitfinex has solid grounds for challenging the prosecution’s accusations and they have been highlighted very well in the Attorney General’s response to the injunction . Before looking into their arguments, however, let’s clarify the patrimonial situation of both Tether and Bitfinex.

In my previous article, I exposed all the clues suggesting that Tether was actually 100% backed, at the time, by U.S. dollars, contrary to what the detractors suggested. The article’s story ended shortly after banks in Taiwan and Wells Fargo closed Bitfinex and Tether accounts, explaining why Bitfinex had deposited billions of dollars of cash with Noble bank which, at the end of 2017, had a balance of 3.3 billion U.S. dollars, compared to 191 million, the previous year. Since June last year, however, many things have changed.

As shown by the chats, problems started with Crypto Capital. However, even Noble bank was not suited to process the incredible number and size of transactions required by Bitfinex. Tether then moved US$1.8 billion to Deltec Bank & Trust Limited in the Bahamas, the new partner of the crypto currency giant, which remains its main bank to this day. The news became public on November 1st, 2018. From November 27, 2018, Tether reopened account verification without relying on third-party payment processors, such as Crypto Capital.

In the meantime, Bitfinex learnt that Crypto Capital’s accounts in Portugal, Poland and the UK have been frozen by various European authorities. At that time Bitfinex’s management was unaware of the reasons for this seizure, even if the suspicion falls to the US authorities. The company is still moving through legal channels with the aim of unlocking the money, which is now 850 million dollars and the exchange starts to be seriously short of money. A counter move at this point is necessary.

Suspending the withdrawals and publicly declaring to the world that it had a temporary hole of US$ 850 million in these circumstances would have been suicide. First of all, because the money in the banks could be returned at any time and the exchange could be given liquidity again. To announce that you are momentarily insolvent, when the next day could resolve the situation, is to shoot yourself in the foot. Holding on and waiting for the funds to be returned seemed more sensible, especially given that it had already happened that the funds were returned, as in the case of the Dutch subsidiary of Crypto Capital, whose funds were unblocked after 112 days. Above all, however, with all the F.U.D. spread by Bitfinex detractors, on a daily basis, for years, publicly declaring solvency problems would sound like an unconditional surrender to all rumors, probably triggering a massive bank run by users, making the situation even worse.

The management of the exchange therefore decides to take various measures:

- Tether Lends Money to Bitfinex

In November 2019, Tether transferred US$ 625 million to Bitfinex, ostensibly to allow Bitfinex to meet its fiat withdrawal obligations. This was an internal transfer between Tether’s account account at Deltec Bank and Bitfinex’s account with the same bank. In return, Bitfinex transferred $US 625 million (in otherwise unusable funds) from its account at Crypto Capital to Tether’s Crypto Capital account. Essentially, a book entry change was made whereby Tether transferred “liquid” dollars and received “temporarily illiquid” dollars, as the latter funds are frozen in accounts held by Crypto Capital.

But there’s more, a second arrangement took place on March 19, 2019: Bitfinex received a line of credit with Tether of up to US$ 900 million with a three-year term and an interest rate of 6.5%. This transaction is secured by a share charge of 60 million shares of iFinex Inc. (d/b/a Bitfinex), DigFinex Inc., the owner of these shares and the holding company that partly owns both Tether and Bitfinex, agreed not to otherwise encumber these shares, in order to secure this transaction.

In its preliminary injunction filed on April 24, the NYAG accuses Bitfinex and Tether of failing to disclose these transactions to its shareholders and clients. The reasons for having taken these actions without announcing them publicly are, however, clear; as previously stated, announcing a temporary deficit of US$ 850 million could have been suicide.

- Risk diversification by investing in securities

After years of struggling in vain to find a safe haven for their customers’ money, it became evident to Tether/Bitfinex that banking relationships can be extremely fragile. From a problem arose this surprising and brilliant solution; controversial though it may be; to use, transparently, (this decision was announced publicly) part of Tether’s reserves to invest in bonds and government bonds, including U.S. government bonds. The choice may seem disconcerting, after all, the company has insisted, since 2014 (the year Tether launched), that every USDT is wholly backed by a dollar in Tether’s reserves. However, owning diversified, and safe, assets gives a company the ability to hedge the need for a fiat deposit account with a bank, which, as we have seen, can be frozen at any time without notice.

An American T-Bill yields 2.5% interest, such returns on large investment amounts, such as those at Tether’s disposal, constitute stellar returns. In periods when there is a lack of liquidity they can be very useful. On the one hand, investing in bonds can involve risks, as a bond’s predetermined maturity date does not allow for an immediate liquidation of said bond for it’s fiat value, which could lead to a liquidity crunch if there are peaks in the requests of user withdrawals. On the other hand, holding bonds is a good way to diversify one’s exposure to the risks of cash, as the maturity of a short-term government bond can be shorter than the time required to obtain the repayment of funds frozen in a bank account.

Among other things, the choice to diversify reserves was also validated by the fact that only a fraction of reserves held by other existing stable coins anchored to dollars can be liquidated immediately. It is logical then, that Tether is now backed 74% by cash and the rest by other less liquid assets.[18]

Ironically, there are US$ 850 million dollars underlying Tether, frozen in various banks, but the respective USDT still move freely from wallet to wallet, from exchange to exchange, and users trade them (at the current exchange rate) at 0.99 cents per USDT for 1 dollar, in short, almost at parity. But why, we wonder, does the value of USDT in the markets remain so resilient and close to the dollar, despite the news of late? The answer is simply that traders do not short USDT, because they consider it risky or otherwise unprofitable. The only reason why USDT would permanently fall below the value of the dollar is if the underlying dollars are not only temporarily frozen, but permanently confiscated by the authorities. To date this condition is highly unlikely and the charges by the Department of Justice of New York are brittle and unfounded.

4 – THE BITFINEX RESPONSE TO THE ALLEGATIONS

Bitfinex has strong arguments against the NYAG injunction, which have been presented by its attorneys to the Supreme Court of the State of New York[19]

First, a preliminary injunction would not usually be granted in the circumstances of this case, let alone an ex parte preliminary injunction. Indeed, the prosecution failed to prove the existence of irreparable damage and identify any New York victim who could have suffered a loss:

“Attorney General has not identified any victim that has suffered any loss”.

Notably, Bitfinex stopped servicing customers in the State of New York and even the United States since August 2018. The news, which at the time made a lot of noise in the crypto community, can be read on the Bitfinex website:

“Bitfinex has decided to stop serving US individual and corporate customers altogether. As of August 15, 2018, no trading or funding services will be available to these users”.

In the footnotes, you can find a link to Bitfinex’s announcements in respect of how U.S. customers can close their account and withdraw all funds. As you can see, Bitfinex specified that all funds left on Bitfinex by U.S. citizens will be considered by Bitfinex as “abandoned property”[20].

That is a fact – we also have numerous direct testimonies that United States citizens had to actually close their account. If you don’t know someone personally, you can read about them anywhere online. Here[21], for example, some traders complain about it and ask for alternatives as reliable as Bitfinex, which has always been known to be a platform which is technically flawless and robust but also very convenient in terms of commissions and percentages of lending and funding.

Second, the prosecution does not denounce the opening of a line of credit between Tether and Bitfinex, which is, itself, completely legal. Rather, it accuses the two companies of not having communicated it to customers and shareholders: “the alleged non-disclosure of that information”. However, Tether updated its terms of service on its website in February, a month before the credit facility arrangement, to add to Tether’s cash reserves, notably, “loans made by Tether to third parties, which could include affiliated entities” (where the affiliated entity is clearly Bitfinex).

“the alleged wrongdoing within the purview of the Martin Act is not the line-of-credit transaction itself, but the alleged nondisclosure of that information. While Bitfinex and Tether do not believe they did anything wrong at any point in time, any failures to timely disclose information to customers or to holders of tether was cured when Tether updated its website over two months ago — long before this proceeding was filed. The ongoing transactions via Bitfinex and Tether are not in any sense fraudulent, nor is the line-of-credit transaction”

In addition, Bitfinex reaffirms the robustness of the Tether/Bitfinex group, specifying the amounts kept in reserve and the full solvency of the company, also demonstrated by the amounts processed daily to/from users without any hitch (I quote cutting and freely adapting, original text in the screenshot):

“Tether’s cash reserves to date amount to $2.1 billion. Between December 2018 and April 29, 2019, average withdrawals amounted to $566,000 per day, with the largest withdrawal of $24.2 million. Although Bitfinex fully draws on Tether’s reserves in USD, these still amount to just under 2 billion, making up 68% of the outstanding tethers [which we can see from coinmarketcap are 2.7 billion USDT]. And it’s all about cash reserves. In addition to these, Tether holds fewer liquid reserves, for a total amount of 100% of the tethers in circulation. Commercial banks operate under fractional reserve and, according to the dictates of the Federal Reserve, they must hold cash reserves representing, at most, 10% of their assets. Tether’s reserves far exceed that threshold, and Tether has never failed to process a single withdrawal request”

Finally, Bitfinex throws a curve-ball at the Office of the NYAG:

“The balance of equites strongly factors Bitfinex and Tether, because the Attorney General’s preliminary injunction was obtained via a misleading application, and serves no purpose except to generate headlines. On the other side of the ledger, the injunction is highly disruptive to Bitfinex’s business, and will only harm the very customers the Attorney General claims to be interested in protecting”

Justice Cohen serving on the Supreme Court, examined the documents and expressed his disappointment in respect of the way the injunction was formulated and the absurdity of the number of documents requested. In addition, he stated the following:

“the preliminary injunction that we have right now is vague, open-ended and not sufficiently tailored to precisely what the AG has shown will cause imminent harm. I think it’s both amorphous and endless.”[22]

The New York prosecutor has argued back saying that, all in all, the scope of the injunction is “narrow” and that it would not have a significant impact on the operations of neither Tether, nor Bitfinex.

5 – EPILOGUE

We are looking forward to the next hearing on this case, which is to be held on May 13. Meanwhile, Bitfinex is not standing still. To solve the liquidity issue, Bitfinex team came up with the LEO token as part of their ICO, or rather, IEO i.e. an Initial Exchange Offering.

Here you find the white paper.

The token seems to have the direct purpose of covering Bitfinex liquidity issues. The company sells LEO tokens in exchange for liquid money (dollars, crypto). When some funds stuck in Crypto Capital banks are recovered, Bitfinex buys back the LEO tokens from the holders and burns them. According to the white paper, this process of repurchasing continues until Bitfinex recovers 95% of all funds now seized. In exchange, the holders have very strong discounts on the Bitfinex fees, plus other benefits. Furthermore, the holders have the possibility to exchange these LEO tokens like if they were an alternative to USDTs, just backed up by the money blocked in the banks.

Thanks to the private placement Bitfinex already collected a value corresponding to 1 billion dollars. Yep, it looks like Merlin made his magic, again.

REFERENCES:

The scene in the cover pictures is taken from this sequence

[1] The Editorial Board (2018-03-25). “The Worst Law in America”. Wall Street Journal. ISSN 0099-9660. Retrieved 2018-05-22. https://www.wsj.com/articles/the-worst-law-in-america-1522014930

[2] https://www.nytimes.com/2003/04/28/business/regulators-finalize-14-billion-wall-st-settlement.html

[3] https://www.bloomberg.com/news/articles/2015-11-10/everything-you-need-to-know-about-the-exxon-climate-change-probe

[4] https://www.bloomberg.com/quicktake/martin-act

[5] http://www.albertodeluigi.com/2018/06/13/tether-audit-subpoena-bitfinex/.

[6] https://www.bizjournals.com/newyork/news/2015/08/12/the-great-bitcoin-exodus-has-totally-changed-new.html

[7] https://www.theverge.com/2018/4/17/17247946/bitcoin-new-york-attorney-general-eric-schneiderman-investigation

[8] https://freeross.org/what-was-silk-road/

[9] https://bitcoinexchangeguide.com/cryptocapital-co-may-be-cryptos-black-swan/

[10] Vedi Reddit su r/Bitcoin, Coinapult

[11] Vedi canale Reddit r/CryptoCurrency su CEX

[12] https://www.coindesk.com/crypto-exchange-quadrigacx-awaits-ruling-on-22-million-in-frozen-funds

https://cointelegraph.com/news/judge-rules-in-favor-of-canadian-bank-in-dispute-with-crypto-exchange

[13] Vedi canale Reddit r/QuadrigaCX

[14] https://www.docdroid.net/wYxaOnX/gerald-cotten-will.pdf

[15] https://www.bloomberg.com/news/articles/2019-02-05/crypto-exchange-founder-filed-last-will-12-days-before-he-died

[16] https://www.manhattanda.org/unicredit-bank-ag-to-plead-guilty-and-pay-316-million-to-das-office-related-to-illegal-transactions-on-behalf-of-nuclear-weapons-proliferator/

[17]

24th april:

https://ag.ny.gov/sites/default/files/2019.04.24_signed_order.pdf

25th april:

https://iapps.courts.state.ny.us/fbem/DocumentDisplayServlet?documentId=vIexA1b0spKOnK_PLUS_ZUGTJ3A==&system=prod

[18] https://www.coindesk.com/tether-lawyer-confirms-stablecoin-74-percent-backed-by-cash-and-equivalents

[19] https://iapps.courts.state.ny.us/nyscef/ViewDocument?docIndex=JcKQms/tM52ywY78HUsInw==

[20] https://support.bitfinex.com/hc/en-us/articles/115003461254-US-Residents-Frequently-Asked-Questions

[21] Vedi canale Reddit r/Bitfinex

[22] https://www.coindesk.com/judge-asks-nyag-to-narrow-scope-of-amorphous-bitfinex-document-request